The Rise of Private Credit

Exploring Venture Debt and Business Development Companies (BDCs)

Table of Contents

1. Key Points

- Private credit refers to debt financing provided by non-bank lenders, typically, though not exclusively, to privately held companies. This type of financing includes a diverse range of debt instruments that are structured outside traditional banking channels, tailored to meet the unique financing needs of borrowers.

- The benefits of private credit include the potential for high income generation and attractive risk- adjusted returns for investors, as well as greater flexibility and bespoke solutions for borrowers. These strategies often outperform traditional credit segments, such as high-yield bonds and leveraged loans, while more effectively addressing the capital needs of many companies.

- Venture lending is a vital part of private credit that meets the needs of rapidly growing companies seeking cost-effective capital alternatives to fuel their growth. It has become increasingly popular among late-stage and growth-stage companies as a minimally dilutive complement, supplement, or alternative to equity financing.

- Business development companies (BDCs) have become significant providers of private credit across the debt capital structure. BDCs are a special form of investment vehicle regulated under the Investment Company Act of 1940 and were established by Congress to stimulate economic development by providing greater access to capital for small and medium-sized businesses. This fund structure provides certain unique benefits to investors through enhanced governance features, financial reporting transparency, tax treatment for both US and foreign investors and SEC oversight. BDCs may be listed on major stock exchanges or exist as permanent private financing vehicles. There are currently 139 BDCs with over $312 billion in assets under management (AUM), investing in small and medium-sized businesses across the country. Of these, 48 are publicly traded, collectively managing $141 billion in assets6. BDCs represent a small but growing percentage of the $1.6 trillion private credit market.1

- The market advantage of BDCs with respect to borrowers lies in the current regulatory environment, which may limit banks’ ability to re-enter the venture lending space. Large banks are often more restricted in their financing products compared to BDCs, making them less competitive in the lending market. This creates opportunities for BDCs and other non-bank lenders to strengthen their position as key providers of debt to growing businesses. Simultaneously, BDCs provide investors significantly more protection and regulatory oversight compared to other private investment vehicles. Venture debt accounts for just one of several forms of lending strategies that BDCs can pursue. Currently, five public BDCs with collective assets of over $8.0 billion represent the main players in the public venture debt BDC space.8

2. Private Credit 101

What is Private Credit?

Private credit refers to debt financing provided by non-bank lenders to public and private companies. It encompasses a diverse range of debt instruments structured outside of traditional banking channels and tailored to meet the unique financing needs of borrowers. This includes direct lending, most commonly in the form of senior secured term loans, mezzanine, and other forms of second lien financing, asset-based lending, distressed debt, special situations, structured credit, real estate financing, and venture/growth debt. Private credit transactions are negotiated directly between the borrower and lender, often offering flexible terms and customization not typically available through traditional bank loans or public debt markets.

- Direct Lending: Direct lending involves providing loans directly from investors or lending institutions to borrowers, bypassing traditional banks. These loans can be used for various purposes, such as funding acquisitions, expansion, working capital, leveraged buyouts, or refinancing existing debt. These loans are typically structured as senior secured first or second lien loans or uni-tranche facilities.

- Mezzanine Financing: Mezzanine financing sits in between senior/senior secured debt and equity and is generally junior or subordinated to senior debt in terms of priority and repayment. Mezzanine financing may combine characteristics of both debt and equity instruments. Mezzanine lenders may have the right to convert their debt into equity if certain conditions are met, and these features can range from being very lender friendly conversion features to very borrower friendly conversion features depending on the quality of the borrower and nature of the financing transaction.

- Asset-Based Lending: Asset-based lending refers to loans secured by a borrower’s assets, such as accounts receivable, inventory, equipment, or real estate. These loans are typically structured as revolving lines of credit and are often used by companies with significant assets but limited access to traditional financing.

- Distressed Debt: Distressed debt involves purchasing the debt of companies experiencing financial distress or bankruptcy. Investors may seek to restructure the debt, acquire ownership stakes in the company, or enforce their rights as creditors to recover their investment.

Special Situations: Special situations financing provides capital to companies in unique or complex scenarios, such as turnarounds, recapitalizations, restructurings, or special events (e.g., M&A, IPOs). - Structured Credit: Structured credit creates customized financing solutions tailored to specific borrower needs. These solutions may involve complex structures, such as collateralized loan obligations (CLOs), collateralized debt obligations (CDOs), or other securitized products.

- Real Estate Financing: Real estate financing involves providing loans to finance real estate acquisitions, development projects, or property refinancing. These loans may be secured by the underlying real estate assets and can range from short-term bridge loans to long-term mortgage financing.

- Venture Debt: Venture debt is typically a senior secured term loan provided to high-growth companies, which primary equity holders, or “sponsors,” are institutional venture capital funds. These companies often have not yet achieved sustainable cash flow due to heavy investments in growth, but they possess substantial enterprise value based on their products, technology, and intellectual property. Venture lenders usually participate in the borrower’s upside equity value through warrants but are minimally dilutive to current equity holders and management when compared to additional rounds of venture capital or other equity financing. As a result, venture debt serves as a complement, supplement, or alternative to equity financing, enabling companies to extend their cash runway without significantly diluting existing shareholders.

The Growth of Private Credit

The global financial crisis of 2008 led to significant disruptions in traditional banking channels, prompting banks to tighten lending standards and reduce their exposure to riskier borrowers in response to significant regulatory and shareholder pressure. This created a gap in the credit market, particularly affecting small and medium-sized businesses and companies with less established credit profiles. Private credit emerged to fill this void, offering flexible and customized financing solutions to borrowers excluded from traditional bank lending.

The prolonged period of low interest rates that followed the global financial crisis and continued through the COVID-19 pandemic further incentivized investors to seek higher yields outside traditional liquid fixed-income investments. Private credit provided an attractive alternative, offering the potential for higher returns compared to public debt markets, while still maintaining relative safety compared to riskier assets like equities.

Today, private credit is a vital source of capital for middle-market companies, which are critical to the

U.S. economy. The private credit market is currently valued at approximately $1.61 trillion and is growing

at an average annual rate of around 10%. By 2029, it is projected to reach $2.6 trillion.1 With banks likely to remain cautious, non-bank lenders may face less competition, leading to more opportunities in private credit.

Who Invests in Private Credit?

Institutional Investors and Wealth Managers Leveraging Private Credit for Portfolio Enhancement:

Institutional investors—such as pension funds, insurance companies, endowments, and sovereign wealth funds—increasingly use private credit to enhance their portfolio returns and reduce market correlation.

Similarly, Registered Investment Advisors (RIAs) and wealth managers incorporate private credit into their clients’ portfolios to achieve specific financial objectives, which could include enhancing returns, reducing market volatility, and improving diversification.

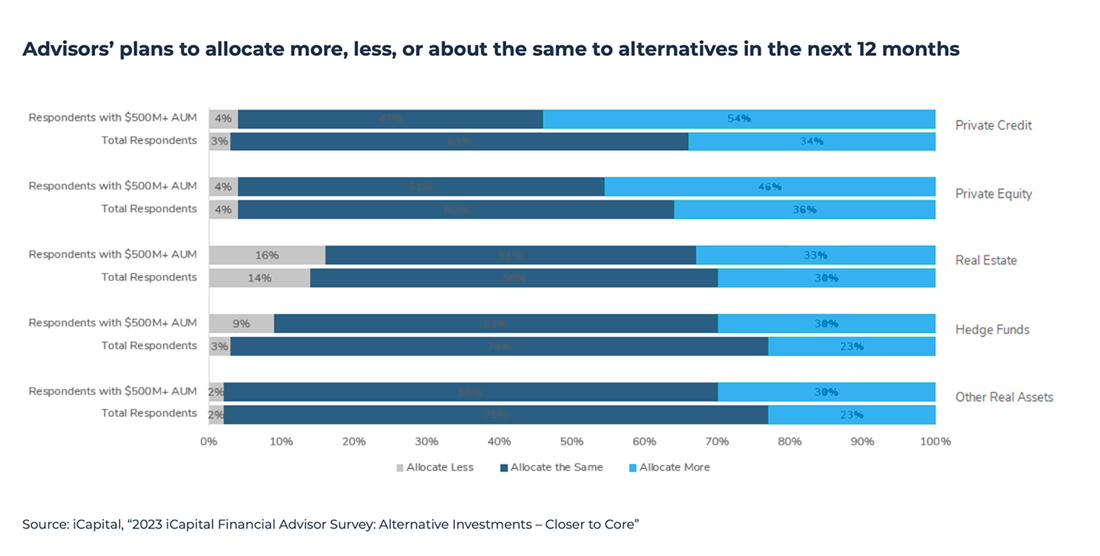

While institutional investors have long been active in the broader alternative investment space—recognizing that alternatives behave differently from typical equity and bond investments and may help lower volatility, provide broader diversification, and enhance returns—there is growing demand from the private wealth segment. According to CAIS2, an investment and technology platform focused exclusively on delivering alternative assets and structured notes to independent financial advisors, a significant shift in portfolio allocation is expected over the next decade, moving from the traditional 60/40 stock and bond model to a 50/30/20 structure, with 20% of portfolios allocated to alternative investments. Alternative investments include venture capital, private equity, real estate, hedge funds, and other assets that fall outside of stocks, bonds, and conventional investment categories. The 2023 iCapital Financial Advisor Survey3 revealed that 95% of financial advisors plan to maintain or increase their allocations to alternative investments in the coming year.

Additionally, 54% of advisors with at least $500 million in assets under management intend to specifically increase their allocations to private credit during this period. Over the next decade, private wealth investor allocation to alternative investments is projected to increase by approximately 12% annually4.

Why Invest in Private Credit?

Advantages of Investing in Private Credit:

- Diversification and Risk Management: Both institutional investors and wealth managers use private credit to diversify portfolios and reduce overall risk. With its low correlation to traditional asset classes like equities and bonds, private credit may help smooth out portfolio volatility and provide a buffer during market downturns. Additionally, its focus on secured loans and strong credit profiles enhances capital preservation and offers downside protection.

- Enhanced Returns and Income Generation: Private credit can be attractive for its potential to deliver higher returns compared to traditional fixed-income investments, making it a valuable tool for achieving better risk-adjusted returns. While this is helpful during most any interest rate environment, it is particularly important in a low-yield environment, where both institutions and individual investors seek alternatives that offer higher yields. For wealth managers, private credit’s steady income streams through interest payments are especially appealing for clients who require regular cash flow, such as retirees. Many major research providers and investment advisors track, index, and publish private credit performance, such as the Cliffwater Direct Lending Index (CDLI) and the Cliffwater Direct Lending Index: Venture-Only (CDLI-V), to support lenders, borrowers, and investors in understanding the risk and returns associated with private credit.

- Access to Niche Opportunities: Both institutional investors and wealth managers leverage private credit to access specialized and often exclusive opportunities not available in public markets. These opportunities include direct lending to small and medium-sized enterprises (SMEs), real estate financing, and distressed debt investments, which can provide attractive returns and allow for more tailored portfolio strategies.

- Inflation Protection and Customization: Private credit investments, particularly those with floating rates, may offer a hedge against inflation, making them a strategic choice in inflationary environments. The flexibility and customization options available in private credit products also enable wealth managers to align investments closely with their clients’ specific financial goals, risk tolerance, and income and cash flow needs.

Overall, investing in alternatives, particularly in private credit, can be an effective strategy for investors seeking to enhance income generation, diversify their portfolios, and manage risk in an ever-changing and challenging investment landscape. The typical floating rate structure of private credit provides protection in a fluctuating interest rate environment, while the due diligence and covenants implemented by private credit managers help wealth managers mitigate risks in their clients’ portfolios.

3. Spotlight On Venture Debt

What is Venture Debt?

Venture debt is a form of debt financing provided to high-growth, venture-backed companies. It is designed to offer capital to companies that may not yet be cash-flow positive or have significant assets to use as collateral, allowing them to extend their runway, fund growth initiatives, or manage working capital needs. Venture debt is typically minimally dilutive, meaning it allows founders and existing shareholders to retain more ownership compared to equity financing.

Differentiating between early-stage venture debt and late-stage venture debt/growth lending

Venture debt falls into two general categories: early-stage and late-stage. For early-stage startups, venture debt can play an important role by filling the gap between equity rounds, extending runway, and giving these companies more time to hit key milestones. In most cases, a lender’s decision to issue venture debt is heavily sponsor-dependent. Due to the inherent risk in early-stage companies, the underwriting is more a function of the quality of the sponsor (the equity investors backing these startups). The underwriting is an assessment of the risk that the sponsor will continue to fund future rounds of equity rather than a thorough evaluation of the business’s financials and model.

In contrast, late-stage venture debt/growth lending is heavily dependent on company fundamentals and less focused on the sponsors. Some lenders also provide debt capital to non-sponsored companies, as well. By this stage, businesses have often reached a certain level of maturity with a clear path to profitability. Lenders focus on revenue, cash flow, and business fundamentals when providing growth capital or refinancing existing debt. Lender risk and credit losses are generally lower at this stage.

How is Venture Debt Structured?

Venture debt is typically structured as a term loan with a duration of three to five years. The loan proceeds can be used for various purposes, including funding working capital, supporting growth initiatives, making acquisitions, or refinancing existing debt. Venture debt often comes with warrants or options that give the lender the right to purchase equity in the company, at a fixed price, providing potential upside if the company performs well. The terms are generally more flexible than traditional bank loans, and the interest rates may be fixed or variable.

Why Do Borrowers Choose Venture Debt?

Borrowers choose venture debt for several reasons:

- Minimally Dilutive Financing: Unlike equity financing, which requires giving up ownership stakes, venture debt provides companies with capital while minimizing equity dilution.

- Extended Runway: It provides additional capital that can extend a company’s operational runway, giving it more time to achieve key milestones before needing to raise additional funds.

- Flexibility: The funds can be used for various strategic purposes, such as fueling growth, making acquisitions, or managing cash flow.

No Requirement for Positive Cash Flow: Venture debt is available to companies that may not yet be profitable, making it a viable option for many high-growth businesses. - Complement to Equity Financing: It can be used alongside equity financing to meet capital needs without overly diluting ownership.

Interest in venture debt has surged, with deal activity in the U.S. more than doubling over the past decade, from $9.0 billion in 2014 to $23.9 billion in 2023, according to Pitchbook5. Founders are increasingly turning to venture debt to fuel growth, particularly in a slower deal environment with unmet demand.

As venture debt continues to gain popularity among high-growth companies, the need for specialized lenders who can provide this type of financing has become increasingly important. This is where Business Development Companies play a crucial role, as they are key providers of venture debt, offering tailored capital solutions to support the growth and development of small and medium-sized businesses.

What is a Business Development Company?

A BDC is a type of investment vehicle that is designed to provide capital to small and medium-sized businesses, typically those that are in the growth or development stage. BDCs were created by the U.S. Congress in 1980 through an amendment to the Investment Company Act of 1940, with the goal of encouraging investment in private companies and small businesses, thereby stimulating economic growth and job creation.

BDCs aim to generate income through yields and seek to provide a consistent dividend by investing in well underwritten debt portfolios. BDCs can also generate income through equity upside in the form of warrants. Unlike traditional VC or PE funds, many BDCs are publicly traded. Currently, there are 139 BDCs, totaling more than $312 billion in assets under management (AUM)6. Of these, 48 are traded on major stock exchanges with $141 billion in aggregate assets, offering individual investors access to investment opportunities that had previously been exclusive to wealthy individuals or institutional investors. BDCs are typically held 50% by individuals, 30% by IRAs, and 20% by institutions. According to Preqin, an investment data company that provides financial data and insight on the alternative assets market, the number of BDCs more than tripled over the past decade7.

Key Characteristics of a BDC:

- Investment Focus: BDCs are specialized investment vehicles designed to provide capital to small and medium-sized businesses, often focusing on those that may not have easy access to traditional financing. These investments typically include a variety of financial instruments such as senior secured loans, mezzanine financing, equity stakes, and hybrid financial products.

- Publicly Traded or Privately Held: Many BDCs are publicly traded on major stock exchanges, allowing individual investors to buy shares and gain exposure to the private debt and equity markets. This public trading provides liquidity and transparency that is not typically available in private equity investments or other forms of private credit, such as traditional LP funds and collateralized loan obligations (CLOs). However, some BDCs are privately held, offering investment opportunities primarily to institutional investors or high-net-worth individuals.

- Regulatory Framework: BDCs are regulated under the Investment Company Act of 1940 but have specific rules tailored to their operations, as established by the U.S. Congress in 1980. For example, BDCs are allowed to use leverage (borrowed money) to increase their investment potential, though they must adhere to certain leverage limits.

- Income Distribution: BDCs are required by law to distribute at least 90% of their taxable income to shareholders in the form of dividends. This makes them similar to Real Estate Investment Trusts (REITs) in terms of their tax structure. Because they distribute most of their income, BDCs avoid paying corporate income tax, passing the tax burden directly to their shareholders.

- Support for Portfolio Companies: Beyond providing capital, BDCs often play an active role in the companies they invest in by offering managerial and operational support. This can include guidance on strategy, financial planning, and governance.

Purpose and Benefits:

- For Companies: BDCs provide crucial financing to companies that might not qualify for traditional loans or equity financing, helping them grow and expand.

- For Investors: BDCs offer individual investors access to a diversified portfolio of private debt and equity investments, along with the potential for high dividend yields due to their income distribution requirements.

Investment Benefits of BDCs:

- High yield, steady/current income: Each BDC distributes its income – made by collecting interest on the loans that it has made to portfolio companies, and from fees it charges those companies – to its investors. Because of their pass-through tax structure, BDCs generally offer higher yields than common stocks.

- Significant liquidity: Some closely held investment vehicles, such as many private equity funds, have shares subject to “lock-up” periods, during which share trading is prohibited. However, just like other products that are offered on the major national exchanges, shares of publicly traded BDCs have no lockups, and can be bought and sold at any time.

- Access to private market opportunities: Through their focus on middle-market companies, BDCs can find and invest in fast-growing innovators and exciting new technologies, opportunities that are not yet widely available.

- Portfolio diversification: Historically, BDCs have a low correlation to other publicly traded asset classes.

- Well-positioned for differing rate environments: BDCs can balance their portfolios with diversified loan structures. Floating-rate loans can be used to take advantage of rising rate environments, while loans may have prepayment penalties and/or interest-rate floors to protect the investment in low-interest rate environments.

In summary, a BDC is a specialized investment vehicle that bridges the gap between small and medium-sized businesses in need of capital and investors seeking exposure to the private market, offering the added benefits of liquidity and transparency. These qualities make venture debt BDCs an attractive option for investors looking to diversify their portfolios and capture the returns offered by the venture debt market.

4. Conclusion and Outlook

The growth of private credit has significantly reshaped corporate financing and capital markets by offering tailored capital solutions that address the evolving needs of small and medium-sized businesses. Private investors through their financial advisors have expanded avenues to invest in these markets and enjoy the investment benefits captured by institutional investors for many years. Venture debt, increasingly popular among high-growth companies seeking minimally dilutive financing, has contributed to the rising prominence of BDCs. BDCs play a key role in providing access to venture and growth debt, helping companies fuel their expansion while offering investors a way to diversify their portfolios and potentially benefit from attractive returns.

As both private credit and venture debt markets expand, investing in BDCs presents a strategic opportunity to capitalize on the growth and innovation driving these sectors.

5. Sources

- Preqin, “Future of Alternatives 2029”, September 2024.

- CNBC, “Advisors are seeing a huge reallocation towards alternative investments: CAIS CEO Matt Brown”, October 2023.

- iCapital, “2023 iCapital Financial Advisor Survey: Alternative Investments – Closer to Core”, August 2023.

- Bain & Company, “Global Private Equity Report 2024,” March 2024.

- Pitchbook, “Q3 2024 PitchBook-NVCA Venture Monitor”

- Small Business Investor Alliance, “About Business Development Companies”, 2024.

- Preqin, “Private Wealth’s Path into US Private Debt”, June 2024.

- SEC, Form 10-6 (RWAY, HRZN, HTGC, TRIN, TPVG), September 30, 2024.